CECL Express is a turnkey, cloud-based solution, designed to provide banks and credit unions with optimized results and reporting that fully meet the ‘Current Expected Credit Loss’ accounting standards.

CECL represents a major change in what is expected from financial institutions in their reporting of, and provisioning against potential credit losses.

Smaller financial institutions are expected to implement forward-looking credit models to estimate losses they may experience.

Selecting inappropriate ‘Expected Credit Loss’ (ECL) models will create a need to hold far more capital than is required, directly causing a loss of Profit and Loss (P&L). Data used within these models must also be reported for audit purposes.

CECL Implementation Considerations

• Banks must pool their loans appropriately.

• Banks must select the most suitable CECL methodology at the pool level.

• Banks may apply location specific qualitative factors to the macro-economic data used within these methodologies.

CECL Express Features

Minimal Implementation Effort

Multiple Expected Credit Loss (ECL) Choices

Comprehensive and Rigorous Audit Support

Best-in-class Intuitive User Experience

Required Market Data Included

Comprehensive and Rigorous Audit

Short Implementation Period

Current Expected Credit Losses (CECL) methodology guidelines require credit unions and banks to adopt the new standard no later than January 2023. Banks and credit unions must start system evaluation, selection and implementation. With this CECL implementation date, they do not have the option to delay this any further.

CECL EXPRESS is a unique industry-lending solution created from the ground up. It is natively integrated with Finastra core systems and requires no other data except the loan portfolio specifics from any bank or credit union. If your underlying loan system is a Finastra core (including Loan IQ, Phoenix, and Ultra Data). Because your loan book is already mapped into the system, users can be up and running on CECL EXPRESS™ within a week. It calculates the provision using multiple CECL methodologies for each individual scenario.

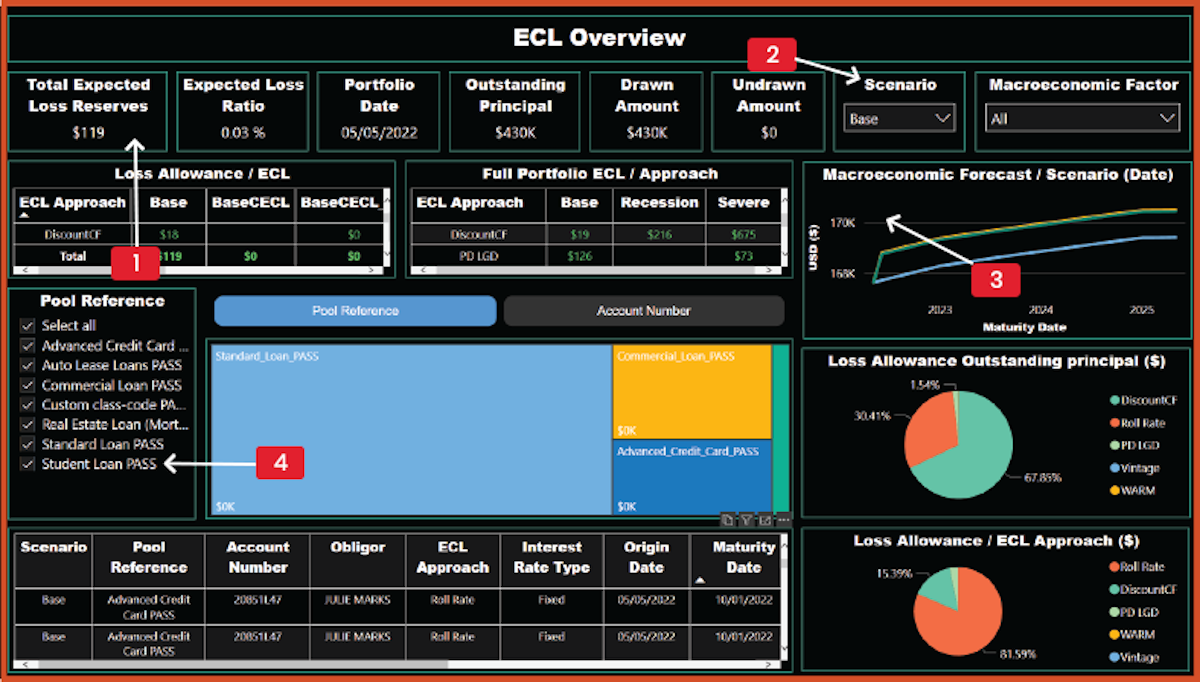

ECL Dashboard

Full CECL result and loan book details

Multiple economic scenarios from base level to severe recession

Macroeconomic factors displayed graphically

Graphical and tabular breakdown of ECL by pool and loan

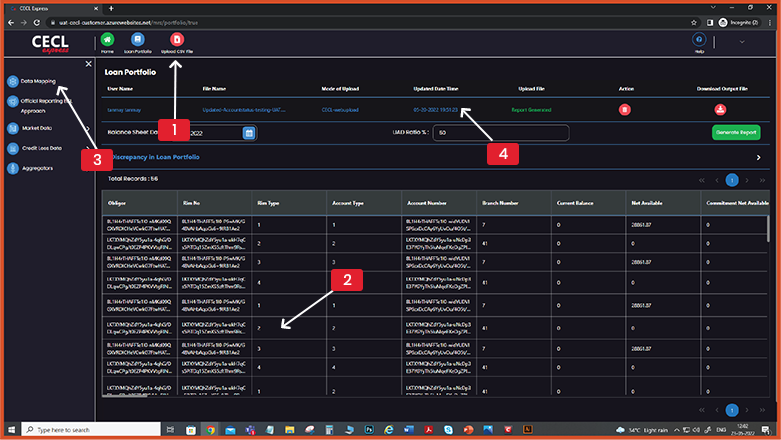

Loan Portfolio Dashboard

Intuitive navigation around the system, for analysis and audit

Full loan details displayed to ensure data integrity

All portfolio data mappings fully explained

Portfolio summary upload details shown for veracity

Multiple METHODOLOGIES

CECL EXPRESS allows maximum flexibility in model choice for adopting the new accounting standard. This enables you to continuously optimize liquidity, P&L and manage capital and required loss provisions.

Banks and credit unions can select from five approved methods:

Vintage

Roll Rae

Discounted Cashflow

Weighted Average Remaining Maturity

Probability of Default/Loss Given Default

As loan portfolios diversify over time, e.g. with inclusion of auto loans and second liens on homes, it is highly desirable to use a targeted method for each loan pool. With CECL EXPRESS, users can assess results for each pool and method, as well as analyze and use them selectively.

Robust Audit Support

Justifying ECL model selection and results to auditors and bank examiners will be the most challenging aspect of complying with CECL requirements. There are two key considerations for supporting effective audit and bank examination functions.

A clear and tractable path and audit trail from ECL results through the underlying data used and loan level result.

Ease of input data management through structural location, access and stepwise analytics.

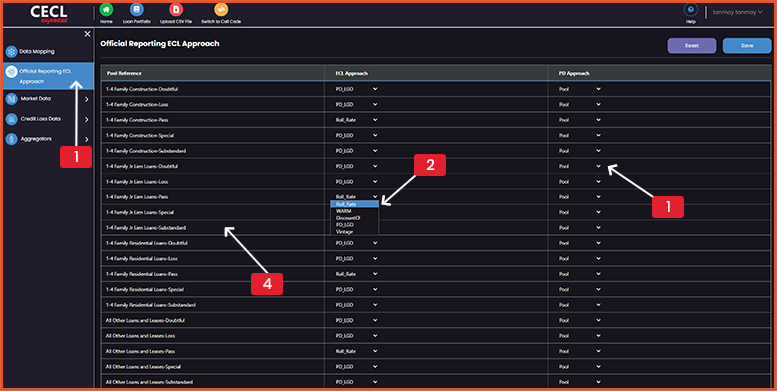

Reporting Dashboard

Dedicated screen for users to select ECL methods by pool

Choice of five approved methods

Choice of five approved methods

Every pool used by the bank listed by call or class code

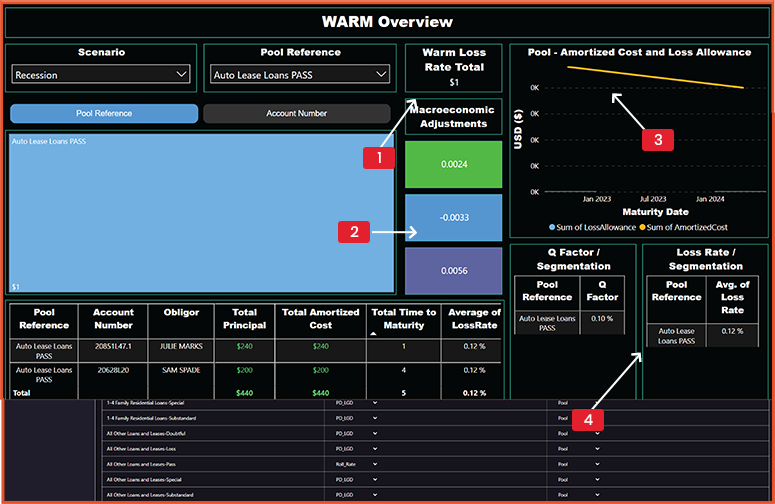

WARM Approach

WARM Overview

Specific results for all pools using the WARM methodology

Macroeconomic factors used in the ECL computation

Graphical representation of amortized cost and loss allowance

Unadjusted loss rate for each pool using the ECL method

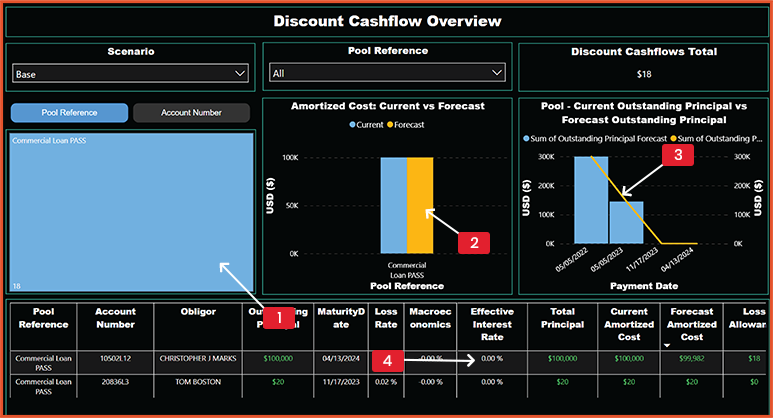

Discount Cashflow Approach

Discount Cashflow Overview

Visual breakdown by pool and account

Amortised cost breakdown of loans using the DCF method

Analysis of loan book by principal

Loan level results including EIR and other contributing calculations

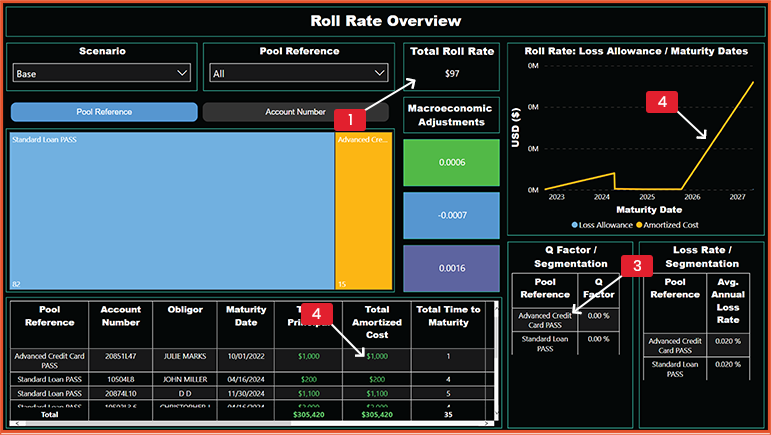

Roll Rate Approach

Roll Rate Overview

Specific results for all pools using the roll rate

Loan by loan breakdown of roll rate specific results

Relevant Q factors applied to the loss calculation

Graphical representation of ECL by loan maturity

CECL EXPRESS is only solution you will need across all functions for complying with the standard/regulation and optimizing capital liquidity.

CECL EXPRESS provides deep dive analysis for each combination of prescribed ECL method and loan pool. This enables senior managements, auditors, and examiners to review and validate the data and results of the CECL analysis.

Provision of all required market data ECL models are only as good as the data that feeds them. It is an imperative for the CECL implementation that all market data used for the audit and supervisory submissions, and that all inputs and results are available and easily tractable.

A CECL EXPRESS system provides the following data elements:

FFIEC/NCUA call reports

Yield curves

PD curves

Peer group losses

Market data needed for all ECL methods

Banks or credit unions have to provide only their specific loan information. This institution-specific confidential portfolio data is viewable on the dashboard for analysis and reporting.

Explore our CECL products and services that help you to analyze and optimize the credit loss data.

ADDITIONAL INFORMATION

Regulatory Sources

FASB: The Financial Accounting Standards Board(FASB) is an independent organization that prescribes financial accounting and reporting standards for public and private companies that follow Generally Accepted Accounting Principles (GAAP). It is recognized by the SEC.

FASB: Financial Instruments-Credit Losses

FASB CECL Q&A

FASB: CECL for small scale Community Banks

FASB: WARM method for CECL

BIS: Bank of International Settlements. The aim of this body is to serve the central banks for monetary and financial stability and foster international cooperation. Fostering discussion and facilitating collaboration among central banks. Supporting dialogue with authorities that promote financial stability. Carry out research on policy analysis. Be a counterparty for central banks in their financial transactions. Serve as an agent or trustee in connection with international financial operations.